Free help: USER GUIDE

Home > Clients & Profits X User Guide > Accounting > General Ledger

|

Clients & Profits X Online User Guide |

Clients & Profits X is built around a one-write, double-entry general ledger. This comprehensive, accrual accounting system automatically tracks your income, costs, and expenses using a custom, user-defined Chart of Accounts. Your G/L accounts track activity totals for 24 accounting periods (15 periods for the Classic edition).

The General Ledger is used for financial accounting. This is different than job accounting, which deals with costs, billings, and expenses from the job’s point-of-view. The General Ledger consolidates all of the work you do -- both job costs and overhead expenses -- to provide a true look at the shop’s net income.

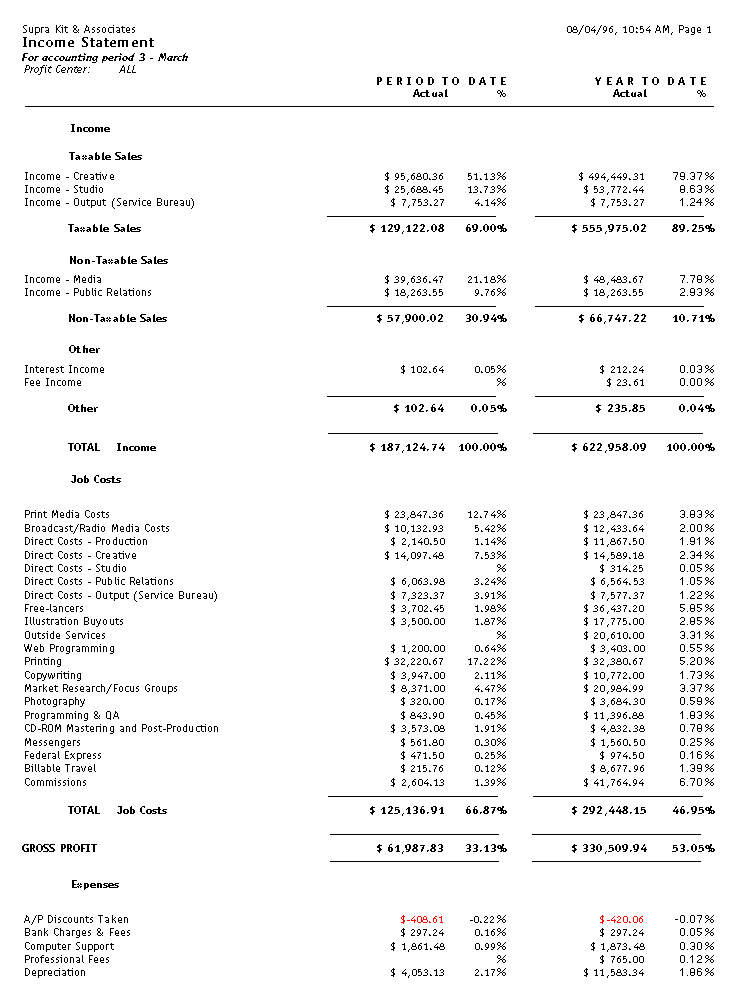

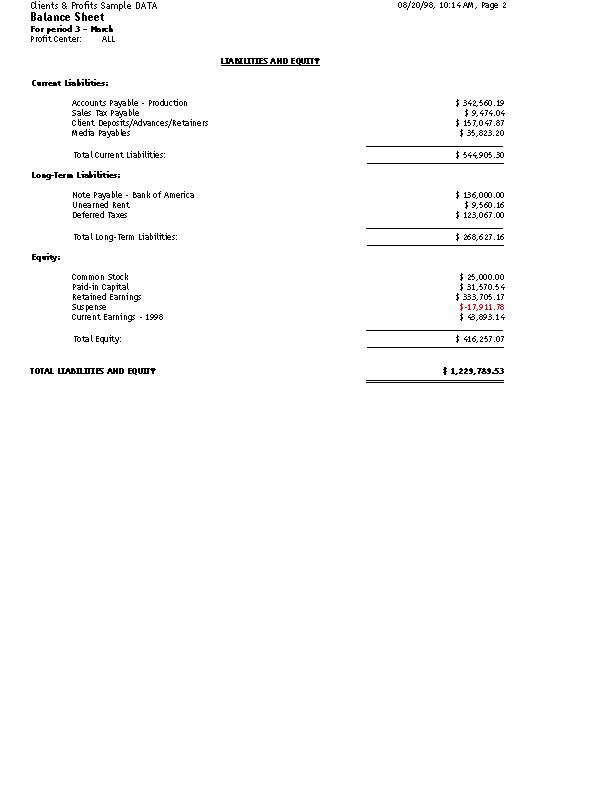

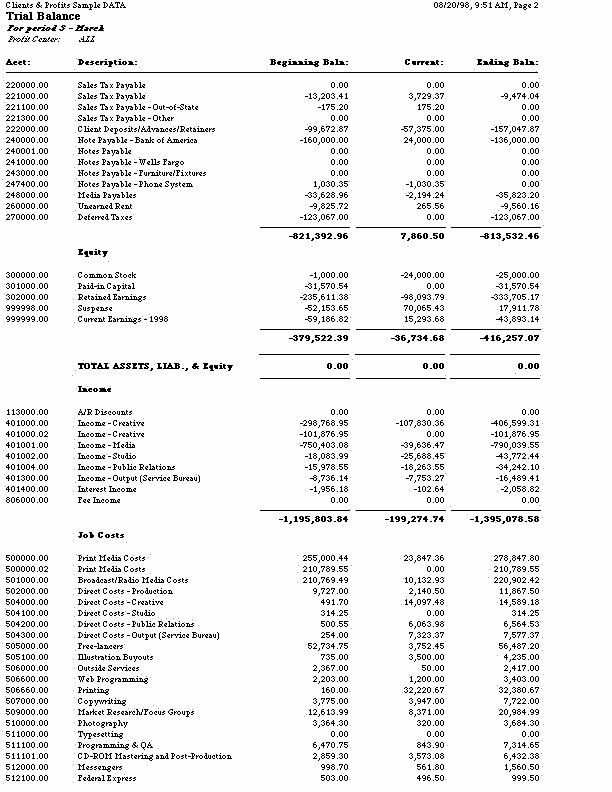

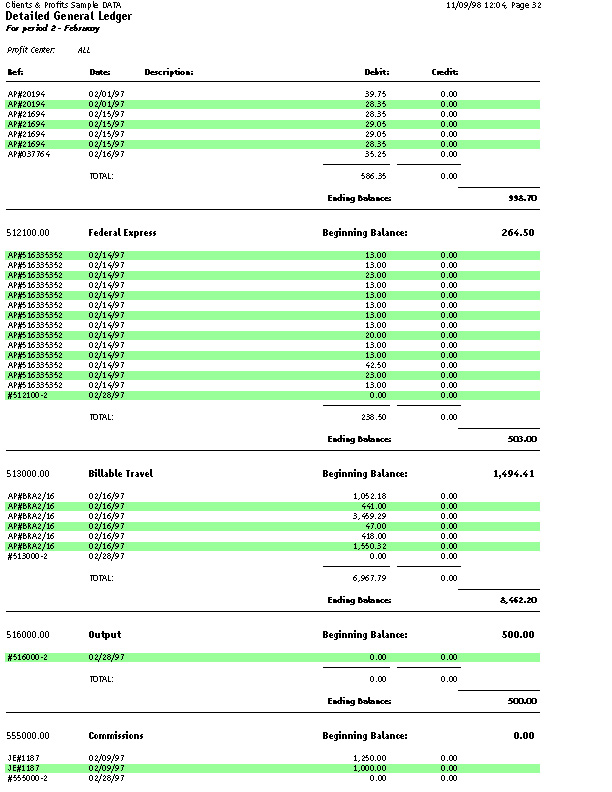

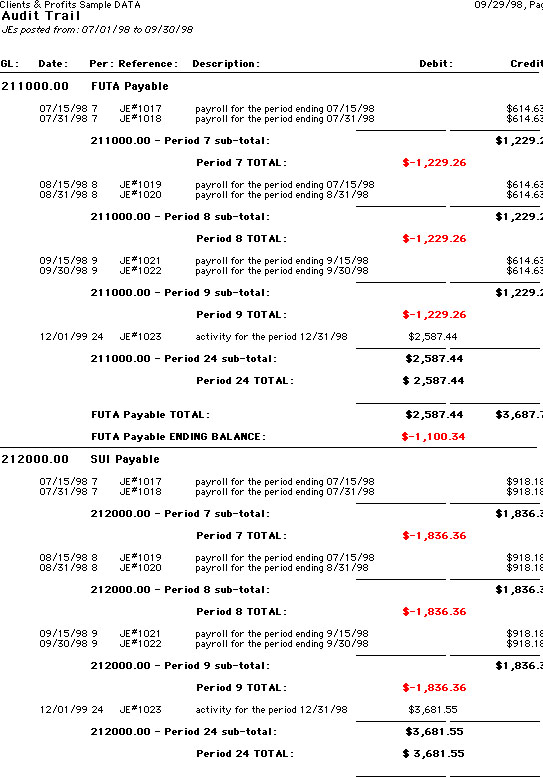

The system provides agency-tailored financial statements, including income statements, balance sheets, trial balances, detailed general ledgers, journals, and audit trails. These reports provide comprehensive auditing and analysis information. Financial accounting takes into consideration

every expense and income dollar in the shop, not just job profitability. Overhead expenses, salaries and miscellaneous income are included on the Income Statement along with job-related transactions. Assets, accumulated depreciation, liabilities, and equity are reported on the Balance Sheet. Audit trails, journals, and ledgers help track the transactions included in the financial statement calculations. General Ledger account budgets are easily added and printed to analyze the account activity more closely.

Unlike other systems you may have used, not everything affects your General Ledger. In fact, only those transactions that involve actual money (such as purchases, checks, and client payments) update the G/L; job costs (such as time, out-of-pocket expenses, and purchase orders) do not affect your financial statements. This is important to understand, since it determines how you’ll manage your books with Clients & Profits.

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

Clients & Profits X has everything you need to produce financial statements, so it replaces any existing accounting systems you may be using. You do not need additional software programs to manage your books.

To use the general ledger

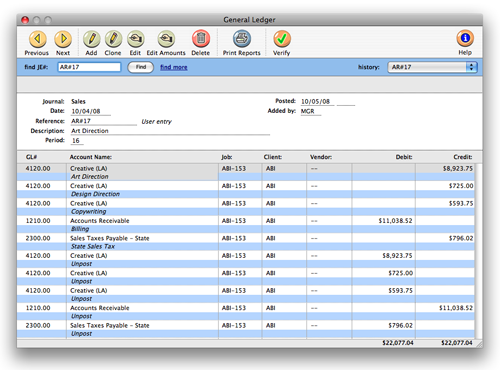

1 Choose Accounting > General Ledger

The General Ledger window opens.

2 Use the find and next buttons to browse through journal entries, or use the find function to search for specific journal entry numbers.

To add a journal entry

General journal entries can be added any time during the month for payroll, insurance expenses, bank fees, etc. That is, anything that doesn't involve Accounts Payable, Accounts Receivable, Client Payments, Checkbook, or Employee Expense reports. Click here for step-by-step instructions.

To clone a journal entry

Cloning makes an exact duplicate of an existing transaction's debit and credit journal entries. You can clone any general journal entry, even from previous periods. Click here for step-by-step instructions.

To edit a journal entry

The Edit G/L Amounts window lists the transaction's debit and credit journal entries. You can edit these amounts by simply typing in the new amounts over the old ones. The total debits must equal the total credits or else your changes won't be saved. Click here for step-by-step instructions.

To delete a journal entry

Only unposted journal entries can be deleted. (Once a journal entry is posted, it can't be deleted -- however, adjusting entries can be made to reverse it or it can be unposted.) Journal entries are deleted by transaction, not by individual entry, to prevent unbalanced entries. Click here for step-by-step instructions.

Verifying Journal Entries

When you highlight a journal entry in the General Ledger window then click the verify button, Clients & Profits will verify the accuracy of the currently displayed journal entry. These journal entries must be posted before verifying. Clients & Profits will not verify unposted JEs. The verify function compares posted entries in the General Ledger against it's source. It will automatically fix any common problems with this posted entry.

|

Cash vs. accrual explained Cash basis and accrual basis accounting are the two most widely recognized methods of tracking a company's income and expenses. The primary difference between the two methods has to do with when the recognition of income and expenses occur. Under the cash method, income is recognized when a payment is received and expenses when a check is written. This method does not let you match revenues generated with the costs associated to them, an important financial accounting concept. Under the accrual method (the one used by Clients & Profits), income is recognized when the invoice is sent to the client (posted) and expenses are recognized when the payable is recorded on the company's books. It's a better way of recognizing income and expenses for financial purposes as it relates the income and expenses more closely to the actual events causing them and gives you the ability to properly match the income generated with the expenses incurred to produce them. |

Using the Out of Balance Checker

It’s possible for your general ledger to become out-of-balance because of system crashes during posting. This happens when one side of a transaction (either a debit or credit) is posted, but the system crashes before the other side is finished. The problem can happen at any time, and it is difficult to prevent (since it is always system related). Find out more about the Out of Balance Checker here.

|

|

|

|

|

Learn more about the general ledger

in this Clients & Profits classroom video training session. Running time: 6:14 |

|

|

|